Are you feeling overwhelmed about selling your house? You’re not alone. As fast home buyers in Minnesota, Mill City Home Buyers understand that the closing process can feel like navigating through a maze of paperwork. The good news is that we’re here to break down everything you need to know about closing documents in simple terms that anyone can understand. Let’s explore what documents you’ll encounter and why they matter when selling your home.

Understanding the Closing Process

The closing process represents the final stage in your home selling journey, where all the necessary paperwork gets signed and ownership officially transfers. Your closing agent will schedule a closing appointment where you’ll review and sign various documents. Most closings take about an hour, though some may require more time depending on your specific situation. The title company will provide several important documents before the closing date to ensure you have time to review them.

During this time, the buyer’s financing will undergo final approval, and the closing agent will prepare all necessary documentation. Understanding the basic steps can help reduce stress and make sure you’re prepared. The title company will work with all parties to ensure all required closing documents for the seller are ready for your review and signature.

What is a Closing Document?

Closing documents include all the legal documents needed to complete your home sale. These documents transfer your ownership rights, outline the terms of sale, and protect all parties involved in the transaction. Each document serves a specific purpose, from confirming your marital status to documenting the payment of any outstanding property taxes and liens.

Key Closing Documents

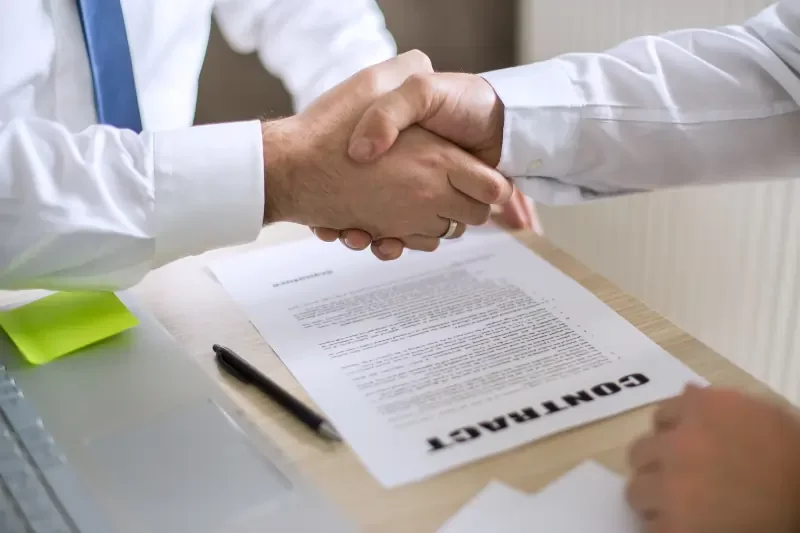

Among the most essential closing documents for sellers is the deed, which serves as your formal transfer of property ownership to the buyer. The affidavit of title, also known as a seller’s affidavit, confirms your right to sell the property and discloses any known issues. You’ll also receive a settlement statement that breaks down all financial aspects of the sale.

The closing statement provides a detailed accounting of all money involved in the transaction, including the sale price and various fees. Your settlement agent will provide closing documents for review before the closing date to ensure you understand all terms. The purchase agreement outlines all terms of the sale, including any personal property in the transaction.

These standard closing documents ensure that both parties understand their obligations and that the property transfer proceeds smoothly. A third-party trustee or settlement agent typically oversees the signing of these documents to ensure everything is properly executed.

Insurance And Title Company Documents

Working with a reputable title company is crucial for resolving potential title issues before closing. The title company conducts a thorough search of public records to ensure you can convey clear ownership of the property. They’ll prepare an affidavit of title and other miscellaneous documents needed to verify there are no existing claims against your property.

As a seller, you’ll need to provide documentation about your current homeowner’s insurance and any claims history. If your property is in a flood zone, you’ll need to disclose this information to the buyer. The title company will also issue title insurance to protect the new owner against any future ownership disputes related to your period of ownership.

Your escrow officer will manage the collection and distribution of these documents, ensuring that all insurance-related matters are properly documented before completing the home sale. They’ll also handle the cancellation of your existing homeowner’s insurance policy and any refunds of prepaid insurance premiums or property taxes from your current escrow account.

Stop Worrying About Closing On Your House And Sell To Us!

We buy your house fast and for cash in Minnesota, without commissions or repairs.

Just fill out the form below or give us a call at: (612) 260-5577 to get your free, no-obligation cash offer!

Reviewing and Signing Closing Documents

During the closing appointment, your closing agent will guide you through each document, explaining what you’re signing and why it’s important. This is when having an experienced real estate attorney can be particularly valuable, as they can help explain any complex legal documents you encounter.

Take your time reviewing the closing documents for the seller. Don’t feel pressured to rush through the signing process – these are important documents that will transfer your ownership rights and have legal implications. If you notice any discrepancies or have questions about the terms of sale, speak up before signing.

The process typically includes signing the warranty deed, various IRS forms, and other required documentation. Your closing agent will ensure all documents are properly executed and ready for filing with the county recorder’s office.

Closing Costs and Fees

Who pays closing costs in MN? This is a common question, and the answer can vary depending on your purchase agreement. Closing costs typically include fees for the title search, real estate attorney, and various other services required to complete the transaction.

When working with Mill City Home Buyers, many traditional seller closing costs are eliminated or covered by the buyer. However, you should still understand any remaining costs early in the process, and your closing disclosure will show the final figures. These costs might include prorated property taxes, recording fees, and any outstanding mortgage payoff amounts.

Understanding these costs upfront helps avoid surprises at closing. A detailed settlement statement will show exactly how the proceeds from your home sale will be distributed, including paying off any existing mortgages or liens.

Proof of Insurance and Property Status

Before your scheduled closing date, you’ll need to provide documentation about your current insurance coverage and declare the property’s occupancy status. This information helps ensure a smooth transfer of ownership and meets title company requirements.

The title company will verify that all necessary documentation is in place and that any existing insurance or tax escrow accounts are properly handled. They’ll also prepare documents for the county recorder’s office to ensure the transfer of ownership is properly recorded in public records.

Your closing agent will verify all documentation is complete and accurate, including any special requirements based on your property type or the buyer’s purchase program.

After Closing

Once you’ve completed signing all closing documents for the seller and the deed has been recorded, you’ll receive copies of everything for your records. Most closings conclude with the transfer of keys and final instructions about canceling utilities and vacating the property according to the agreed-upon timeline.

What is a closing statement for a seller?

The closing statement, also known as the settlement statement, is a detailed document that provides final details about the sale proceeds and closing costs. It’s one of the most important closing documents for sellers because it shows exactly how much money you’ll receive from the sale and how various fees and payoffs are being handled.

FAQ: Important Information For Home Sellers

What happens with the buyer’s loan documents during closing?

When selling your home, you should understand that buyers working with a mortgage lender will have specific requirements. Their loan application and loan estimate must be processed before closing. However, when selling to Mill City Home Buyers, you avoid delays related to loan terms or mortgage applications since we purchase with cash.

How do buyer financing requirements affect sellers?

Traditional buyers often need to provide proof of mortgage insurance premiums, and flood insurance, and demonstrate that the home will be their primary residence. Their mortgage broker will verify the loan amount and interest rate. With Mill City Home Buyers, you can skip these complications since we don’t need lender approval.

What documents will buyers need to sign?

Buyers typically sign a promissory note, security instrument (like a deed of trust or mortgage note), and various loan documents. Their mortgage lender intends to verify all of these during the home-buying process. As a seller to Mill City Home Buyers, you avoid waiting for these steps.

What timing issues should sellers know about?

In traditional sales, buyers must receive certain documents three business days before closing. Their monthly payment details, purchase price, and escrow items need verification. When you sell to Mill City, you don’t have to worry about loan terms or due dates delaying your closing.

What role does the title company play?

The title company helps transfer titles and handles tax declaration requirements. While they’ll work with a buyer’s real estate agent and mortgage broker in traditional sales, Mill City Home Buyers simplifies this process by handling most paperwork directly.

What makes selling to Mill City Home Buyers different?

Unlike traditional buyers who need to coordinate with a mortgage lender, verify loan documents, and wait for loan application approval, we buy houses in St. Paul with cash. This means you can avoid delays related to mortgage insurance premiums, flood insurance requirements, or escrow items. Contact us today to learn how we can make your selling process simpler and faster.

Conclusion

Navigating closing documents for sellers doesn’t have to be overwhelming. If you’re saying “I’m ready to sell my home fast now Minneapolis“, consider working with a professional cash buyer like Mill City Home Buyers. We simplify the process by handling most of the paperwork and offering quick closings.

Understanding these important documents is crucial for protecting your interests during the sale. As cash home buyers, we pride ourselves on making the process transparent and straightforward. We believe in explaining each step clearly so you know exactly what to expect.

Remember, when you need to sell your house quickly and efficiently, Mill City Home Buyers is here to help. Visit our About Us page to learn more about our company and how we calculate our offers. Want to skip the traditional real estate process entirely? Contact us today for a no-obligation cash offer on your home.